Why I like purple spaghetti

For high net worth investors, risk management is NOT relative, and not a game.

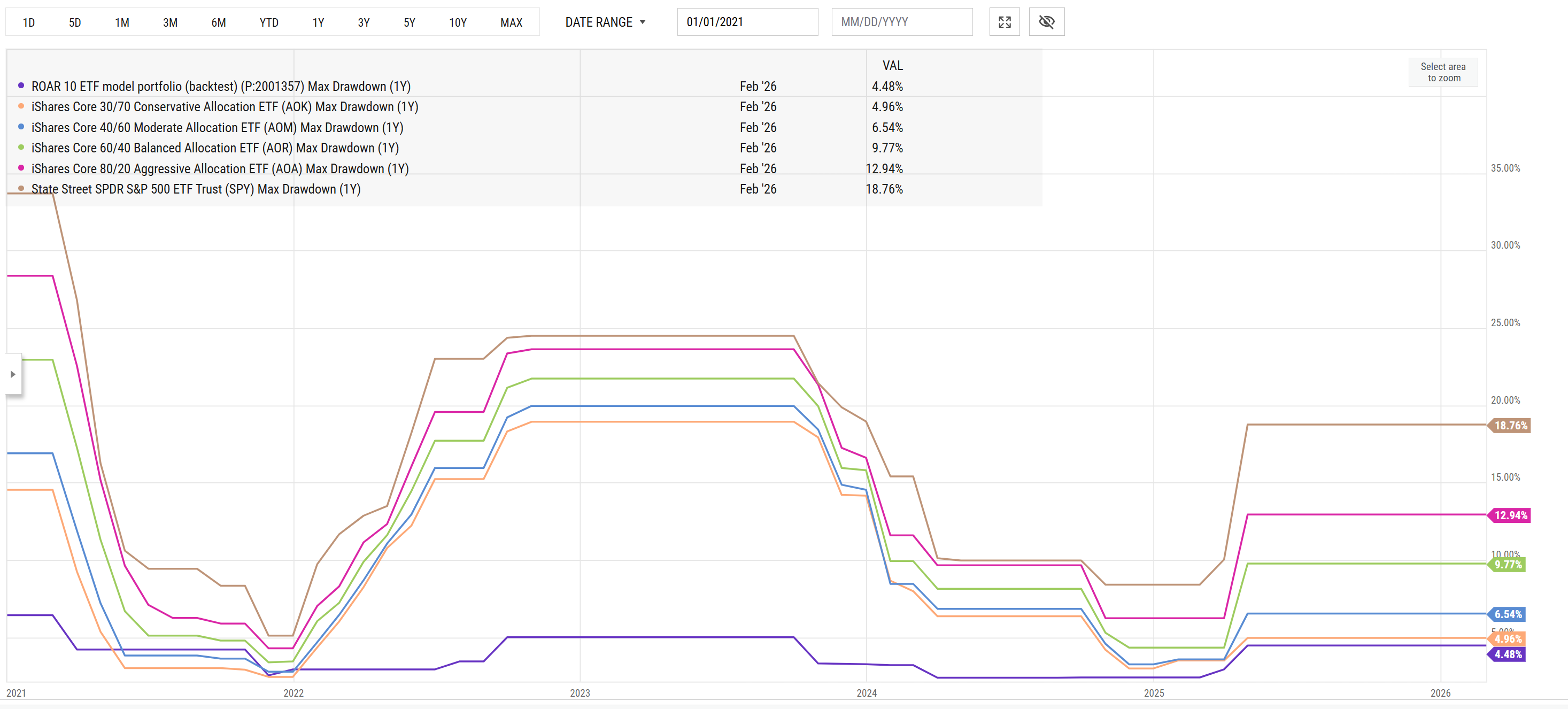

That’s a colorful chart right there, isn’t it? Now, what the heck does it mean? It is my favorite type of graph, because it shows “rolling” results.

Too often we are presented with snapshots of past performance, whether back-tested like this one for my ROAR ETF model portfolio, or live. That is, we are shown “past 1, 3, 5 year returns.” That leaves out all of the events in between. For years, some professional investors have used that to their advantage. In an era where the typical market dive has been relatively brief, those snapshot performance charts can easily hide what happened during the worst of times.

Because in the decades I’ve been investing professionally, I’ve come to realize something that I sense many newer investors have not been told. That while the return percentage an investment generates is wildly inconsistent, the ability of an active strategy to manage risk tends to be much more consistent.

For example, if you see an ETF or a portfolio strategy made 14% a year the past 5 years, the worst assumption you can make is that level will persist. However, if a portfolio did a nice job of managing risk in a period where the stock market, bond, market or both fell, that should prompt a very valuable question: “what is it about that investment process that allows it to do that? And how likely is it to be repeated in future market cycles?”

That essentially sums of my old job. My very old job, that is. When I first started managing other people’s money in the mid-1990s, I was allocating among a fixed set of funds or “separately managed account” strategies, run by active managers. I did not have the wide reach I afford myself now, in terms of researching and identifying ETFs and stocks to own and trade as I wish.

I was a “manager of managers.” I spent years wearing the hat of “director” as opposed to being the active manager myself. It didn’t long before I realized, after being a manager scout for a half decade, that I could be my own portfolio manager. And do so on behalf of my then-firm’s clients, as I was the Chief Investment Officer (CIO).

Fast-forward to today: I am thrilled to be able to help self-directed investors and investment advisors find their own way to managing money like a pro.

OK Rob, get to the purple spaghetti part already…

That’s why I write posts like this. And why I’ll now explain the “purple spaghetti” reference. That chart shows the “maximum drawdown” over the past year. As the chart goes from left to right, the 1-year period keeps “rolling” with it. So the far right end of the graph is the worst drawdown (peak to trough loss in % terms) over the 12 months ended yesterday.

My ROAR 10 ETF portfolio, which was the subject of this research paper discussed earlier this week is that purple line. And I highlighted not simply because this is the main ETF portfolio I now oversee for my own family, but because it was specifically designed to manage risk first.

It is doing the job lately, as paid subscribers know. And since it is now largely an automated process (I review and finalize the ROAR Score-driven model weights generated every Wednesday for the copy-trading version of it offered at PiTrade.com) it is, I think the purple line is relevant.

It shows that the 5% max drawdown I aim for, even in some very sudden market drops (20-34% during that 2020-current period, the brown line above) is potentially achievable. More importantly to me, ROAR 10 did not have worse-case scenarios anywhere near those of the spectrum of asset allocation ETFs shown in the graph.

Just in the past 6 years, the uber-popular 60/40 portfolio (60% stocks/40% bonds), the green line above, has had max drawdowns of 23%, 22% and 10% at separate times. I like bonds, but I built a bond hedge into ROAR 10, in addition to the equity hedges and cash, because that market is also riskier than it has been in decades. And, more opportunistic.

So yeah, I like purple spaghetti. That’s why I built a modern, flexible, model portfolio of 10 ETFs around that risk management concept. As noted above, generating positive returns is often not the challenging part of investing.

Avoiding giving a lot of those gains back in down market stretches, costing time and emotional energy? THAT is the challenging part. We try to help investors be up for that challenge, at all times.